IDR 39,944,307,174

DOWNLOAD SEKARANG

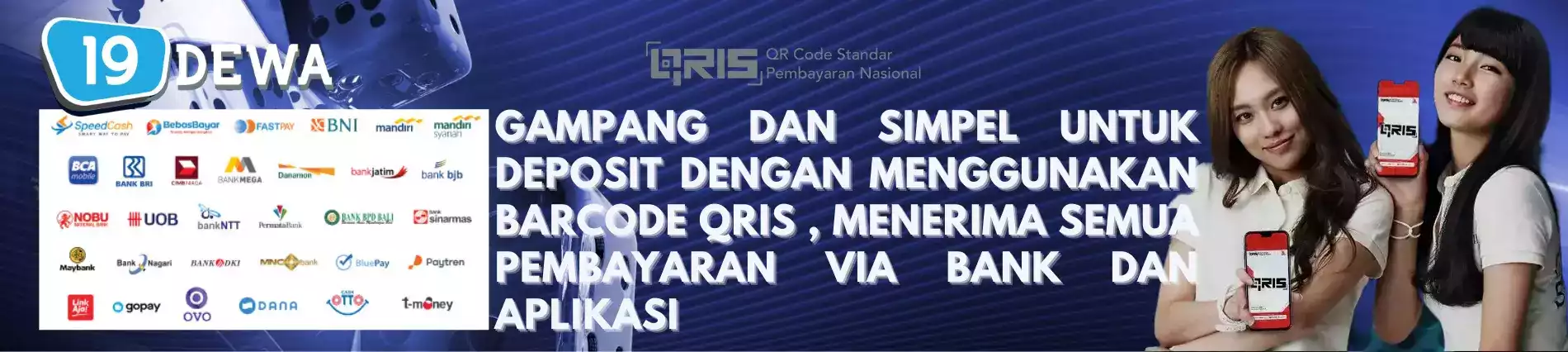

Layanan Member

Tambah Dana

Waktu

Menit

WITHDRAW

Waktu

Menit

Sistem Pembayaran

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

OFFLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

ONLINE

19DEWA Tempat Paling Asyik Nongkrong Layanan Care 24 Jam